Source: (Macrotrends, s/f).

Source: (Macrotrends, s/f).

DOI: https://doi.org/10.34069/AI/2024.82.10.9

How to Cite:

Baboyan, K.L. (2024). Assessment of solvency-liquidity relationship in food and meat producing organizations. Amazonia Investiga, 13(82), 112-123. https://doi.org/10.34069/AI/2024.82.10.9

Assessment of solvency-liquidity relationship in food and meat producing organizations

Արժութային և լիկվիդության հարաբերության գնահատում սննդի և մսի արտադրող կազմակերպություններում

Received: April 2, 2024 Accepted: May 25, 2024

Written by:

Khachatur Levon Baboyan

https://orcid.org/0000-0002-3672-732X

Ph.D., student at the M. Kotanyan Institute of Economics, Candidate of Economic Sciences. Financial Director of Finance, Martin star LLC., Armenia. WoS Researcher ID: HKE-1566-2023

Abstract

Cash flow management in commercial organizations of the production sector is one of the key problems of financial management in the post-crisis stages of the pandemic and its overcoming, which requires new solutions.

This article presents practical solutions for improving financial management in the context of liquidity-solvency relationship, cash flow, and current asset valuation in six leading companies that produce food and meat products by capitalization listed on the world stock exchange and studied.

Since the role of artificial intelligence is highly valued in the current period, financial management professionals have also started to use various learning forecasting models in order to increase the efficiency of their decision-making.

Forecasting the capital structure in commercial organizations with an artificial intelligence model is a completely new approach in the financial management system, the main task of which is to define the preferred ratio of the components of liabilities in connection with the minimum cost of capital.

Keywords: food, meat, cash flow, listed company, machine learning model, stock market, capital, assets, liabilities, net income, current, assets, net cash flow, liquid cash flow, financial management, liquidity, solvency, operational risk.

Ամփոփում

Արտադրական ոլորտի առևտրային կազմակերպություններում դրամական միջոցների հոսքերի կառավարումը համաճարակի և դրա հաղթահարման հետճգնաժամային փուլերում ֆինանսական կառավարման առանցքային խնդիրներից է, որը պահանջում է նոր լուծումներ։

Այս հոդվածում ներկայացվում է իրացվելիություն-վճարունակություն հարաբերությունների, դրամական միջոցների հոսքերի և ընթացիկ ակտիվների գնահատման համատեքստում կապիտալիզացիայով ուսումնասիրված վեց առաջատար ընկերություններում գործնական լուծումներ ֆինանսական կառավարման բարելավման համար, որոնք արտադրում են սննդամթերք և մսամթերք՝ և ցուցակված են համաշխարհային ֆոնդային բորսայում:

Քանի որ ներկա ժամանակաշրջանում արհեստական ինտելեկտի դերը բարձր է գնահատվում, ֆինանսական կառավարման մասնագետները նույնպես սկսել են օգտագործել ուսուցման կանխատեսման տարբեր մոդելներ՝ իրենց որոշումների կայացման արդյունավետությունը բարձրացնելու համար:

Արհեստական ինտելեկտի մոդելով առևտրային կազմակերպություններում կապիտալի կառուցվածքի կանխատեսումը լիովին նոր մոտեցում է ֆինանսական կառավարման համակարգում, որի հիմնական խնդիրն է որոշել պարտավորությունների բաղադրիչների նախընտրելի հարաբերակցությունը կապիտալի նվազագույն արժեքի հետ կապում.

Հիմնաբառեր: սնունդ, միս, դրամական հոսքեր, ցուցակված ընկերություն, մեքենայական ուսուցման մոդել, ֆոնդային շուկա, կապիտալ, ակտիվներ, պարտավորություններ, զուտ եկամուտ, ընթացիկ, ակտիվներ, դրամական միջոցների զուտ հոսքեր, դրամական միջոցների հոսք, ֆինանսական կառավարում, իրացվելիություն, վճարունակություն, գործառնական ռիսկ.

Introduction

In modern conditions, the management of own current assets of commercial organizations is directly characterized by the ratio of long-term and short-term sources of financing: considering the provision of a favorable level of profitability as the primary goal, the formation of the necessary conditions for the financial stability, liquidity and normal solvency of the organization. Due to this, the choice of the type of policy for the formation of own current assets depends on the direction of the organization's financial policy, profitability-risk, and solvency-liquidity relations.

The Covid-19 pandemic has had a significant impact on the solvency and liquidity levels of commercial organizations in the manufacturing sector. Due to the massive spread of the pandemic, many EU entities, especially in mining and retail, have started to show signs of insolvency due to low revenue levels and large cash outflows (Chang, Gan & Mohsin, 2022).

Therefore, in practice, there is a need to restructure the structure of sources of financing current assets of organizations within the framework of financial policy, as a result of which the priority task is to neutralize the risk of insolvency.

Inventory, trade receivables, short-term financial investments, and cash and cash equivalents are key components of current assets when developing approaches to increasing solvency. In particular, Karim, R., Mamun, M.A.A. & Kamruzzaman, A.S.M., examining 18 years of data from all sectors of Bangladesh and using the GMM estimation model, in the results obtained by their research, they confirmed the point of view that by minimizing the amount of stocks, the shelf life of the finished product, improving the collection of receivables and extending the repayment period of payables as much as possible can have a significant positive impact on the profitability of Bangladeshi companies. In particular, the unfavorable structure of capital allocation was highlighted as one of the key issues (Karim, Mamun & Kamruzzaman, 2023).

This point of view also highlights the urgency of finding new solutions to the problem of not only forming the preferred structure of capital for organizations, but especially predicting the rational structure of its allocation in current assets.

According to the research results of N. Aktas, E. Croci & D. Patmezas, the hypothesis was put forward according to which the companies in which there is an optimal level of working capital policy and those companies, that approach that optimal level (increasing or decreasing their investment in working capital), practically improve their inventory levels and operational management performance (Aktas, Croci & Petmezas, 2015).

The current asset and current liability turnover management policy of a food and meat producing organization is also directly related to the formation of a rational capital structure, which at the current stage is necessary for the creation of sufficient reserves of liquidity and solvency of the balance sheet.

It should be noted that in the post-crisis phase caused by the pandemic, efficient, predictive scenarios-based solutions for the development and application of new approaches are required in order to implement effective interrelated control of solvency and liquidity in large organizations producing food and meat products. This determines the relevance and importance of the research carried out on the example of the leading organizations of the food and meat producing sub-branch.

Review of literature

Effective financial management is extremely important for the sustainable development of any organization. Researchers Charli Sitinjak, Anne Johanna, Buschhaus Avinash, Bevoor Bevoor conducting a comprehensive analysis of financial management: as a network of interconnected processes, studied the function of financial management within the organization and its role in the context of achieving financial optimization (Sitinjak et al., 2023).

At the current stage, within the framework of financial management directions, new research solutions are connected with the problems of financial security of organizations: emphasizing liquidity, required return on equity, desired level of solvency in relation to debt service. In particular, Lita C. Megasanti, Hedwigis Esti Riwayati put forward the point of view with the results of joint research, that institutional ownership in companies in the construction sub-sector facilitates the acquisition and financing of companies by both lenders and investors, thereby increasing the liquidity of the construction company. However, increasing the level of liquidity is used not only for the purpose of the company's activities, but also for its political interests. In terms of improving the efficiency of solvency management, the acceleration of the collection of receivables was emphasized.

Hoang Bui and Zoltan Krajcsak studied the effect of corporate governance on the performance of the companies' financial indicators, particularly financial results, for publicly listed companies in Vietnam for the period 2019-2021. According to the obtained results, companies mainly focus on making decisions that are in the best interests of shareholders, which increases the value of these companies to investors, thereby contributing to the improvement of the company's value (Bui & Krajcsak, 2023).

In the context of the solvency-liquidity relationship, Jessica Medeline Effendie, Henny A. Manafe, Stanis Man in their joint research tried to find the main determining factors at the current stage, with which liquidity indicators affect the solvency of the organization from the point of view of the fulfillment of financial obligations. By studying the behavior of the current liquidity ratio (current assets/current liabilities) it was revealed that the high value of the latter, especially in the case of a high proportion of cash in current assets, has a negative impact on profit (Effendie, Manafe, & Man, 2022).

Hussain, Rana Yassir; Wen, Xuezhou; Hussain, Haroon; Saad, Muhammad suggest using long-term debt to manage insolvency risk in listed real sector companies in Pakistan. They hypothesized that debt repayment decisions are more important than capital structure decisions because they are directly related to insolvency risk (Hussain et al., 2022). In the framework of this article, we will try to refute this hypothesis by applying the results of our predictive machine learning model for predicting capital formation (Baboyan, 2021), (Baboyan, 2022).

Note that machine learning models are gradually gaining primary importance in new approaches to financial management. Specifically, Zong-De Shen & Suduan Chen developed a financial condition assessment and forecasting model based on hybrid machine learning technology. This study applied several machine learning technologies. First, important variables were screened using artificial neural networks (ANNs). Then, prediction models were built based on decision tree C5.0 and random forest (RF). According to the empirical result, the ANN-RF model provided higher accuracy (Shen, & Chen, 2022).

In their research, Annisa Nafatul Jannah, Hasim As'ari aimed to reveal the relationship between solvency-liquidity-profitability in audit frameworks using data from 180 organizations in the energy sector, combining quantitative research methods and a number of analytical tools (Jannah, & As’ari, 2023). The results of this research revealed that liquidity and solvency variables have no effect on audit delay (their significance values are greater than 0.05).

J. M. Effendie, Henny A. Manafe, S. Man have given significant importance to financial ratios in the analysis of solvency and liquidity on the financial condition of Indonesian companies, that they are useful for recording the financial health of the company at the current stage or in the future (Effendie, Manafe, & Man, 2022).

As for the solvency-liquidity correlation management through current financial demand liquidity bands, then scenario solutions were proposed by researchers Professor A. Matevosyan, L. Hovakanyan, M. Matevosyan and A. Grigoryan's joint research (Matevosyan et al., 2023). The components of determining the current financial requirement used in this approach are also directly applicable from the point of view of calculating the liquid cash flow index.

Taking into account the existing approaches regarding the solvency-liquidity relationship within the framework of financial management, within the framework of this article, the main goal is to propose a methodological and interrelated optimization approach as a new solution direction in leading food and meat producing organizations with capitalization listed on the international stock exchange.

Research methodology

A study of various approaches to financial management shows, that the control of solvency and liquidity of commercial organizations, (Megasanti & Riwayati, 2023) within its framework, there are various methodological approaches, especially in terms of current assets and liabilities components, their turnover evaluation, cash flow calculation. (Van Horn, & Wachowicz, 2008).

Causal assessment identified significant factors on earnings per share of listed consumer goods companies in Nigeria Gilbert Ogechukwu Nworie; Vitalis O. Moedu; By Onyali, Chidiebele Innocent Current Assets, Inventory Turnover Ratio, Cash Ratio (Nworie et al., 2023).

Within the framework of the research, we offer new methodological solutions.

KCLG= KCLT/ KCAT, (1)

With further modification we will have:

KCLG= , (2),

Where:

KCLT - is the current liabilities turnover ratio,

KCAT -is the current asset turnover ratio,

TCL- is the growth rate of current liabilities in the reporting period,

TCA -is the growth rate of current assets in the reporting period.

The importance of the proposed approach comes down to:

LCF=( short term loans + long term loans - Cash on Hand) reporting period –(short term loans + long term loans-Cash on Hand) previous stage (3)

We suggest calculating the formula as follows:

LCF=( Current Liabilities + long term loans - Cash on Hand) reporting period –(Current Liabilities + long term loans - Cash on Hand) previous stage (4):

The importance of including total current liabilities in the calculation formula of LCF is justified by the fact that they have a direct impact on the current solvency of a specific commercial organization and are limited only to the index of long-term loans, in practice, short-term loans causing problems in terms of current solvency, purchase payables, received advances, and short-term tax payables to the budget are ignored.

Recommendations aimed at improving the solvency-liquidity relationship for the studied organizations producing food and meat products are presented.

Results and discussion

Among the leading international food and meat producers listed on the stock exchange, the first four are Tyson Foods (37-year share price history), Hormel Foods (33-year stock price history); JBS SA (52 years of share price history), Pilgrim's Pride (36-year stock price history) and top-six Beyond Meat (4-year stock price history); Steakholder Foods (2-year stock price history) has a long history and is distinguished by its distinctive traditions.

Food production is considered the process of turning raw materials into edible food. The food production process includes various stages, cleaning, processing, separation and ends with packaging and marketing.

Meat is an important source of food for many people around the world. The global demand for meat is growing: meat production has more than tripled over the past 50 years. Now more than 340 million tons (Ritchie, Rosado & Roser, 2019) are produced in the world every year.

Within the framework of this article, our main goal is to highlight the existing problems in the process of solvency and liquidity management in food and meat producing organizations and to propose new approaches to their related control.

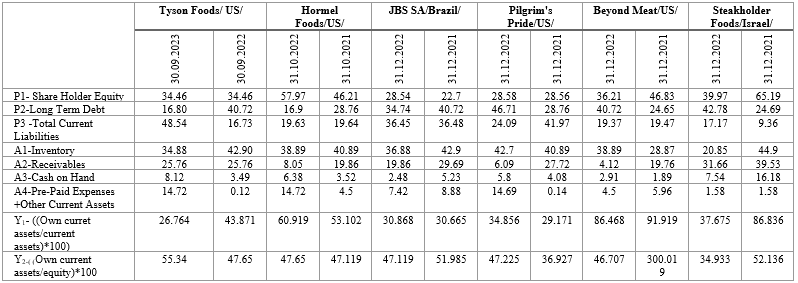

Step 1. As shown in Food Items - Meat Products - Top Stocks (Macrotrends, 2023).

the analysis of the relative weights of the main components of current assets(inventories, trade receivables, cash, other current assets) and liabilities (equity, non-current liabilities, total current liabilities)in total assets in the listed and studied food and meat producing organizations, then, especially in the last five years, there is a structurally irrational picture of JBS SA, Beyond Meat and Steakholder Foods among the top six companies listed on the stock exchange that produce food and meat products.

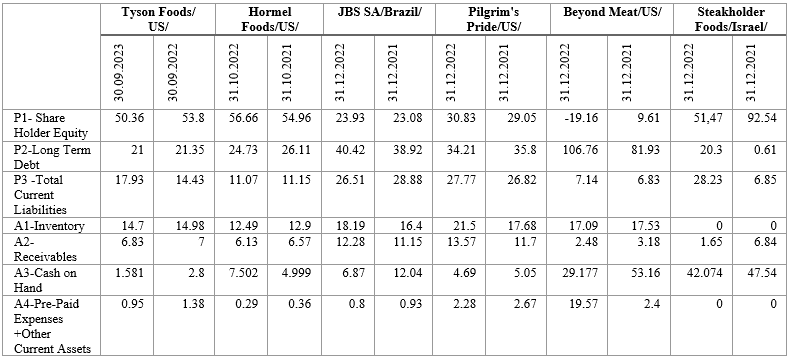

The behavior of the specific weights of the components of current assets and liabilities in the studied organizations is presented in table №1.

The data in Table No. 1 show that among the studied organizations, JBS SA, Beyond Meat Steakholder Foods have a problem of rationalizing the capital structure; the problem of low cash turnover is also evident in the last two. In the other three leading organizations, we will consider the effectiveness of financial management in the context of the use of the best option of capital.

Table 1.

The behavior of the shares (%) of current assets and liabilities components in listed organizations producing food and meat products

Source: (Macrotrends, s/f).

Step 2. We present the results of the new calculation approach for the current liquidity ratio used for the purpose of liquidity assessment in table №2.

Table 2.

Current liquidity ratio with the proposed new calculation approach in listed organizations producing food and meat products

Behavior

The mathematical trend of the feasibility factor calculated with the new approach R2 assessment values for 2019-2023. the best behavior was recorded in JBS SA Brazil: R2 = 0.65 and Pilgrim's Pride US: R2 = 0.61; Organizations Hormel FoodsUS R2 = 0.26 and Beyond Meat US R2 = 0.27 took similar values. Irregular liquidity management behavior was observed in the organization Tyson Foods USR2 = 0.01. As for the Steakholder Foods Israel organization, calculations using this method were not made due to the lack of required data.

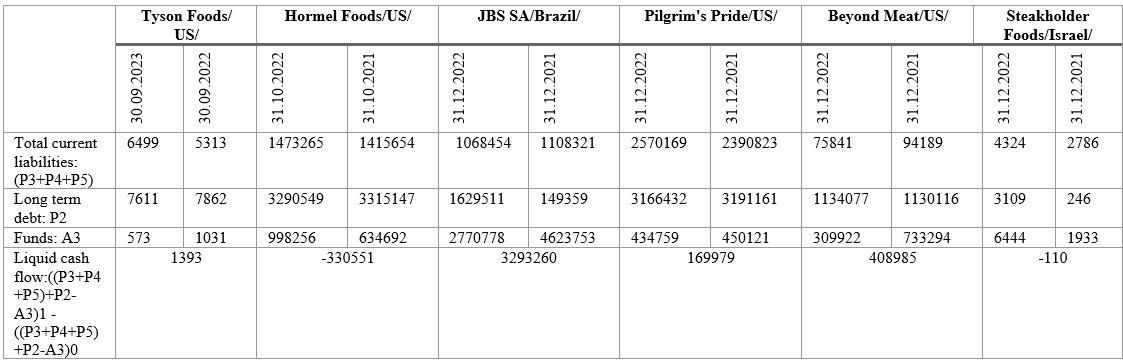

Step 3. The calculated values of Liquid cash flow index proposed for solvency assessment are presented in table № 3.

Table 3.

The comparison of the liquid cash flow indicator with the proposed new calculation approach in listed organizations producing food and meat products

Insolvency problems were revealed in the organizations Hormel FoodsUS and Steakholder FoodsIsrael with the values of the liquid cash flow indicator determined on a new methodological basis. In particular, at the Steakholder Foods/Israe/ organization, based on the results of the analysis of table №2, a crisis is revealed in the context of the solvency-liquidity relationship. As for the Hormel FoodsUS organization, again based on the results of the analysis of table No. 2, there is a pre-crisis situation in relation to solvency-liquidity. In the other four studied organizations, according to the liquid cash flow indicator, a normal solvency level was recorded, which we will try to improve based on the results of the sixth step forecast.

Step 4. The solvency assessment is presented in Table № 4.

Table 4.

Sum assessment of solvency in listed organizations producing food and meat products

The sum assessment of solvency, according to the mathematical trend, received the highest value in the organization Tyson Foods US: R2 = 0.95. Pilgrim's Pride US: R2 = 0.56 and Hormel FoodsUS: R2 = 0.51 were relatively stable from the point of view of solvency. The pre-crisis state of solvency according to the monetary assessment was recorded in JBS SA BrazilR2 = 0.24 organization, and the crisis state in Steak holder Foods Israel R2 = 0.032 and Tyson Foods US R2 = 0.0006 organizations. It should be noted that the Steakholder Foods Israel organization is very poor in terms of financial solvency.

By combining the results of the third step, the SteakholderFoods Israel organization is in a critical state of solvency.

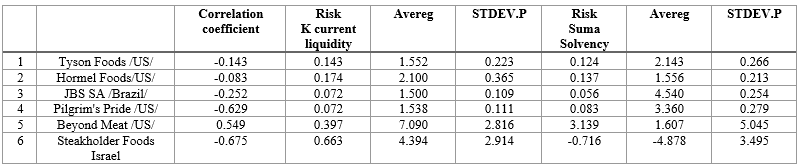

Step 5. Calculations revealing the correlation between the liquidity ratio determined in the second step and the solvency sum estimate determined in the fourth step and the risk (standard deviation/average size) are presented in table №5.

Table 5.

Correlation and risk between the liquidity ratio and the solvency ratio in listed companies producing food and meat products

According to the results of the assessment of the fifth step, a noticeable negative relationship between solvency and liquidity was recorded in Pilgrim's Pride /US, Beyond Meat US and Steakholder Foods Israel/ organizations. In Tyson Foods US, Hormel Foods US and JBS SA Brazil, there is a weak correlation between the liquidity ratio and the solvency ratio. In terms of the liquidity factor, the risk in the studied organizations was manageable: RiskK current liquidity<1. As for the monetary assessment of solvency, organizations Beyond Meat US and Steakholder Foods Israel/ were assessed as risky.

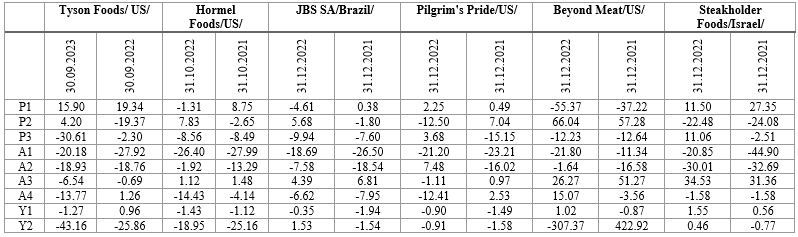

Step 6. Changes in actual and predicted values are presented in Table No. 6.

Table 6.

Changes in the actual and forecasted values of the shares of the main components of liabilities and the components of current assets

Note that in the studied organizations, the values of input variables Y1, Y2 suggested by the results of three-step prediction of the model are either close to the actual values, or have undergone a certain improvement trend.

Based on the best option, we have presented the results of the machine learning model prediction of the capital structure in table №7.

Table 7.

Predicted values (%) of current asset and liability component shares in listed organizations producing food and meat products, according to the best option

Source: (Macrotrends, s/f).

Source: (Macrotrends, s/f).

According to the results of the forecast, Hormel FoodsUS: 2023, JBS SABrazil2023, Beyond MeatUS and 2023 and 2022, Steakholder FoodsIsrael: 2023 had a problem of equity capital.

According to the predictive results of the model, it is recommended to reduce the P3 component in 2023 in all six studied organizations.

The reduction of the P2 component in the 2023 model was considered appropriate by Tyson FoodsUS, Hormel FoodsUS, JBS SABrazil, Beyond MeatUS. In Steakholder FoodsIsrael organization, from the point of view of prioritizing the current solvency, the model proposed the addition of the P2 component.

Regarding the main components of current assets, the need to change the proportions of stocks (A1), trade receivables (A2) and cash and their equivalents (A3) was recorded. Basically, the optimization of cash flows in food and meat producing organizations is recorded as a problem of primary regulation in connection with solvency-liquidity.

Note also that due to the specifics of their technological chain, increasing the efficiency of inventory control is also considered a significant factor in the solvency-liquidity link.

Step 7. Prediction results. Based on the results of the sixth step for the studied food and meat producing organizations, the predicted values of the liquidity ratio, solvency sum assessment and liquid cash flow index are presented in table № 8.

Table 8.

Forecast results of liquidity ratio, solvency assessment and liquid cash flow index in listed food and meat producing organizations/2023/

The forecast data presented in Table No. 8 document that there have been significant changes in the solvency-liquidity relationship in terms of selected indicators. In particular, the decrease in the values of the liquidity ratio determined by our proposed adjustment contributed to the improvement of the solvency position. In all five organizations (Calculations were not performed for Steakholder Foods Israel due to lack of necessary data), the liquidity ratio values decreased somewhat in accordance with the best-case projected capital structure. In this sense, it becomes possible to use the liquid reserves more rationally to solve the solvency problem.

From the perspective of monetary assessment of solvency, it was most effective in Tyson Foods US and Beyond Meat US.

The predicted values of the sum assessment of solvency in the studied organizations Hormel FoodsUS, JBS SA Brazil and Pilgrim's Pride US are very close to the actual values.

The concept of management of internal or external financial relations adopted in a specific commercial organization must correspond to the approved charter and the nature of strategic goals. As the main goals of forming the financial policy and management mechanism, obtaining the maximum profit by strengthening competitive positions in the market and, as much as possible, preventing threats to the development of the organization, in particular, the risk of insolvency and the possible risk of bankruptcy, are emphasized.

In terms of the Liquid cash flow index, the values of default liabilities and current assets components for organizations have definitely contributed to the increase of the solvency level, which is an important achievement in the solvency-liquidity relationship.

In order to solve the existing financial problems in the organizations, it is very necessary to improve the efficiency of working capital management, to carry out mandatory monitoring of liquidity in the context of the connection with other components of the financial situation through newly developed systems, which will make it possible to avoid new financial difficulties to a certain extent and to develop a realistic, accurate financial strategy for development.

Conclusion

In the course of the research, we proposed a new methodological solution for evaluating the solvency-liquidity relationship, which were considered in the context of the direct relationship between increasing the level of solvency by forecasting the capital structure, using liquid reserves, and allocating funds more rationally.

Effective management of solvency-liquidity relationship in food and meat exporting organizations requires multi-faceted and in-depth study, which is essential, especially in terms of capital structure forecasting solutions.

Bibliographic References

Aktas, N., Croci, E., & Petmezas, D. (2015). Is working capital management value-enhancing? Evidence from firm performance and investments. Journal of Corporate Finance, 30, 98-113. https://www.sciencedirect.com/science/article/abs/pii/S0929119914001606?via%3Dihub

Baboyan, K. (2021). Approach for Predicting Index of Security with the Own Current Assets according to the Capital Structure of Commercial Organizations of the Republic of Armenia. Bulletin of the Georgian National Academy of Sciences, 15(2), 185-190. http://science.org.ge/bnas/t15-n2/26_Baboyan_Economics.pdf

Baboyan, K. (2022). Improvement-Based Approach for Control over Solvency of Commercial Organizations in the Context of Prediction of Preferred Capital Structure. Transition Studies Review, 1, 65-82. https://doi.org/10.14665/1614-4007-29-1-004

Baboyan, K. (2023). New approach to the prediction of the structure of liabilities in commercial organizations. Pacific Business Review (International), 15(8), 54-64. http://www.pbr.co.in/2023/February7.aspx

Bocharov V.V., & Leontev, V.E. (2004). Corporate Finance. SPb.: Peter, 504-562 https://www.studmed.ru/bocharov-vv-leontev-ve-korporativnye-finansy_029474e.html

Bui, H., & Krajcsák, Z. (2023). The impacts of corporate governance on firms’ performance: from theories and approaches to empirical findings. Journal of Financial Regulation and Compliance, 32(1), 18-46. https://acortar.link/v17lnm

Chang, L., Gan, X., & Mohsin, M. (2022). Studying corporate liquidity and regulatory responses for economic recovery in COVID-19 crises. Economic Analysis and Policy, 76, 211-225. Doi: 10.1016/j.eap.2022.07.004

Effendie, J. M., Manafe, H. A., & Man, S. (2022). Analysis of the Effect of Liquidity Ratios, Solvency and Activity on the Financial Performance of the Company (Literature Review of Corporate Financial Management). Dinasti International Journal of Economics, Finance & Accounting, 3(5), 541-550. https://dinastipub.org/DIJEFA/article/view/1507/1058

Hussain, R. Y., Wen, X., Hussain, H., Saad, M., & Zafar, Z. (2022). Do leverage decisions mediate the relationship between board structure and insolvency risk? A comparative mediating role of capital structure and debt maturity. South Asian Journal of Business Studies, 11(1), 104-125. https://www.emerald.com/insight/content/doi/10.1108/SAJBS-05-2020-0150/full/html

Jannah, A. N., & As’ari, H. (2023). The influence of liquidity, profitability and solvency on audit delay in energy sector companies listed on the idx in 2020-2022. Journal of Economics, 12(04), 2396-2402. https://ejournal.seaninstitute.or.id/index.php/Ekonomi/article/view/3154

Karim, R., Mamun, M.A.A., & Kamruzzaman, A.S.M. (2023). Cash conversion cycle and financial performance: evidence from manufacturing firms of Bangladesh. Asian Journal of Economics and Banking, 8(1). https://doi.org/10.1108/AJEB-03-2022-0033

Macrotrends (s/f). Alcoholic Beverages - Top Stocks. https://www.macrotrends.net/stocks/industry/19/alcoholic-beverages

Macrotrends (2023). Food Items - Meat Products – Top Stocks. (2023, December 21). Retrieved from https://www.macrotrends.net/stocks/industry/75/food-items---meat-products

Matevosyan, A. V., Hovakanyan, L. Y., Matevosyan, M. H., & Grigoryan, A. Z. (2023). The Proposed Approach to Current Financial Requirement Management in Organizations of The Alcoholic Beverages. Journal of Law and Sustainable Development, 11(12). https://doi.org/10.55908/sdgs.v11i12.1721

Megasanti, L. C., & Riwayati, H. E. (2023). The Effect Of Liquidity, Profitability, And Solvency On Financial Distress With Good Corporate Governance As A Moderation. International Journal of Economic Studies and Management (IJESM), 3(1), 398-408. https://doi.org/10.5281/zenodo.7740329

Mukaka, M.M. (2012). Statistics Corner: A guide to appropriate use of Correlation coefficient in medical research. Malawi Medical Journal, 24(3), 69-71. https://www.ncbi.nlm.nih.gov/pmc/articles/PMC3576830/pdf/MMJ2403-0069.pdf

Nikolova, L.V. (2015). Risk Management of Innovation Projects in the Context of Globalization. International Journal of Economics and Financial Issues, 5(3), 73-79. https://www.econjournals.com/index.php/ijefi/article/view/1692/pdf

Nworie, G. O., Moedu, V. O., & Onyali, C. I. (2023). Contribution of Current Assets Management to the Financial Performance of Listed Consumer Goods Firms in Nigeria. International Journal of Trend in Scientific Research and Development, 7(1), 77-87. https://acortar.link/M0ZQXJ

Ritchie, H., Rosado, P., & Roser, M. (2019). Meat and dairy production. Our world in data. Retrieved from: https://ourworldindata.org/meat-production

Shen, Z. D., & Chen, S. (2022). Financial Distress Prediction: A Hybrid Tracking Model Approach. Asian Journal of Economics, Business and Accounting, 22(24), 185-192. https://journalajeba.com/index.php/AJEBA/article/view/906/1811

Sitinjak. C., Johanna. A., Avinash. B., & Bevoor B. (2023). Financial Management: A System of Relations for Optimizing Enterprise Finances – a Review. Journal Markcount Finance, 1(3), 160-170. https://doi.org/10.55849/jmf.v1i3.104

Van Horn, J. C., & Wachowicz, J. M. (2008). Fundamentals of Financial Management. 13th Edition. England: Prentice Hall. https://acortar.link/i3QjuE

https://amazoniainvestiga.info/ ISSN 2322-6307

This article presents no conflicts of interest. This article is licensed under the Creative Commons Attribution 4.0 International License (CC BY 4.0). Reproduction, distribution, and public communication of the work, as well as the creation of derivative works, are permitted provided that the original source is cited.