DOI:https://doi.org/10.34069/AI/2021.48.12.27

Features of the formation of incomes of the consolidated budgets of the constituent entities of the Russian Federation

ОСОБЕННОСТИ ФОРМИРОВАНИЯ ДОХОДОВ КОНСОЛИДИРОВАННЫХ БЮДЖЕТОВ СУБЪЕКТОВ РОССИЙСКОЙ ФЕДЕРАЦИИ

Gilnara Rashitovna Nigmatullina114

Abstract

The article examines the features of the formation of incomes of the consolidated budgets of the constituent entities of Russia on the basis of a statistical assessment of the dynamics and structure of incomes of the consolidated budget. The study provides a comparative assessment of changes in budget revenues and their structure in indicative years 2005, 2010, 2015 and 2019, which makes it possible to identify the main trends and features of the formation of revenues of the consolidated budgets of the Russian Federation and regions of the Central Federal District in different time periods. Over the past 5 years, the growth rate of the revenues of the state budget of the country has decreased in comparison with previous periods, which is associated with the deterioration of the economic situation due to the economic crisis. Comparison of the growth rate of Russia's GDP with the growth rate of income for the main types of taxes made it possible to establish that taxation in the sphere of business is growing at a faster pace than the economy. In the context of the regions of the Central Federal District, significant differentiation remains, both in the absolute value of the volume of budget revenues, and in the specific weight of one or another type of taxes. The overwhelming share of budget revenues comes from personal income tax, the volume of receipts of which is growing most dynamically, as a result of which in 2019 its share varied from 21% to 40% by region.

Key words: Russian Federation, state budget, revenues, taxation system, personal income tax, corporate income tax.

Аннотация

В статье рассматриваются особенности формирования доходов консолидированных бюджетов субъектов России на основе статистической оценки динамики и структуры доходов консолидированного бюджета Российской Федерации в целом и в разрезе регионов Центрального федерального округа. В исследовании дана сравнительная оценка изменений доходов бюджета и их структуры в индикативных 2005, 2010, 2015 и 2019 годах, что позволяет выявить основные тенденции и особенности формирования доходов консолидированных бюджетов Российской Федерации и регионов Центрального федерального округа в разные периоды времени. За последние 5 лет темпы роста доходов государственного бюджета страны снизились по сравнению с предыдущими периодами, что связано с ухудшением экономической ситуации в связи с экономическим кризисом. Сравнение темпов роста ВВП России с темпами роста доходов по основным видам налогов позволило установить, что налогообложение в сфере бизнеса растет более быстрыми темпами, чем экономика. В разрезе регионов Центрального федерального округа сохраняется значительная дифференциация, как по абсолютному значению объема доходов бюджета, так и по удельному весу того или иного вида налогов. Подавляющая доля доходов бюджета приходится на налог на доходы физических лиц, объем поступлений которого растет наиболее динамично, в результате чего в 2019 году его доля варьировалась от 21% до 40% по регионам.

Ключевые слова: Российская Федерация, государственный бюджет, доходы, налоговая система, подоходный налог с физических лиц, корпоративный подоходный налог.

Introduction

In accordance with the principles of state structure, the budget is the most important component of the country's economic mechanism, since it forms the financial basis for the activities of state bodies and the implementation of socio-economic policy. The main functions of the state budget include the accumulation and redistribution of financial resources, through which also support and stimulate the development of various spheres of the country's economy (Geys, & Sørensen, 2020). Fiscal policy in Russia is an important element in the framework of financial policy, since it determines the economic course of development of the state and takes into account its interests, thereby shaping the socio-economic and tax policy (Levkina, Loksha, & Mokhireva, 2020). The importance of the formation of an effective budgetary policy is to create, first of all, financial prerequisites for solving the most important tasks facing the state. In addition to financial support for solving current state issues, social policy is important, which is often one of the most problematic areas, since in conditions of a budget deficit, resources for the implementation of social projects are insufficient (Zyukin, Bystritskaya, Golovin, & Vlasova, 2020). In this regard, the formation and increase of the revenue side of the state budget in modern conditions, associated with its deficit, becomes an important task.

The revenue side of the federal budget of Russia consists of tax and non-tax revenues, while tax revenues today form the basis of the revenue side of the country's budget. This is natural, since in the context of political instability in previous years and the onset of another economic crisis against the backdrop of the coronavirus pandemic, the country's foreign trade activity suffered significant damage, which negatively affected the country's income from this type of activity.

The main type of taxes that form the budget revenues of the Russian Federation is value added tax (VAT), the share of which in the total volume of budget revenues today is about 40%. Also significant are tax revenues to the federal budget from the mineral extraction tax, export customs duties, corporate income tax and excise taxes.

Since Russia is the largest oil and gas exporter, there is a consideration of the structure of the revenue side of the budget of the Russian Federation in the context of the origin of income - oil and gas and non-oil and gas. As a result, despite the active export of oil and gas resources, the share of this type of income in the overall structure of the country's budget revenues is only one third, while non-oil and gas revenues account for about 70%. This confirms the fact, despite the importance of the oil and gas sector for the country, it is not the main source of replenishment of the revenue side of the state budget.

In accordance with the principles of the federal structure of Russia, the budgetary system is multilevel, while the composition of the revenue side of the federal and regional budgets is different. This is due to the fact that certain types of taxes are exclusively federal, while others are regional or local. In addition, the revenues of the consolidated budgets of the regions of the Russian Federation include gratuitous receipts, which include interbudgetary transfers, mainly from the federal budget - subsidies, subventions, grants and other types (Lavrovsky, & Goryushkina, 2021).

The growth of the country's budget revenues directly depends on the degree of favorable economic situation, since this creates the preconditions for the intensification of the production and economic activity of enterprises, the growth of their turnover, wages of workers and, accordingly, the volume of taxes and deductions transferred (Bashar & Bashar, 2020). Therefore, today, in the context of an economic downturn and a depreciation of the ruble, exacerbated by the onset of the coronavirus pandemic, the country's budget system has also been negatively affected by a decrease in both tax and non-tax revenues of Russia. This, among other things, is due to structural and sectoral problems in the economy, since today there are few industries in the country showing dynamic growth, which has a positive effect on filling the state budget (Zemtsov, 2020).

Methodology

It is proposed to study the features of the formation of incomes of the consolidated budgets of the constituent entities of the Russian Federation on the basis of a statistical assessment of the dynamics and structure of incomes of the consolidated budget of the Russian Federation as a whole and in the context of the regions of the Central Federal District. The work used statistical data from the collections “Russia in Figures” and “Regions of Russia. Socio-economic indicators "on the amount of income of the consolidated budgets of the Russian Federation and the regions of the Central Federal District in current prices (Federal Service State Statistics, 2020a; Federal Service State Statistics, 2020b). In the course of the study, a comparative assessment of changes in budget revenues and their structure in indicative years 2005, 2010, 2015 and 2019 is given, which makes it possible to identify the main trends and features of the formation of revenues of the consolidated budgets of the Russian Federation and regions of the Central Federal District in different time periods.

At the first stage, the change in the income of the consolidated budget of the Russian Federation as a whole, its structure by main types of income, primarily tax, is investigated, and the growth rate of the country's budget revenues by type of income is compared with the growth rate of GDP (in value terms); this makes it possible to assess what is growing more dynamically - the economy or the volume of tax collection.

At the second stage of the study, the dynamics of incomes of the consolidated budgets of the Central Federal District regions is assessed in the context of the main types of taxes (corporate income tax, personal income tax (PIT) and property tax) and an analysis of changes in their share in the total income of the respective budgets. This makes it possible to identify structural transformations in the system of forming the revenue side of the consolidated budgets of the Central Federal District, namely, to determine in the direction of which type of taxes the main emphasis has shifted.

Results and discusion

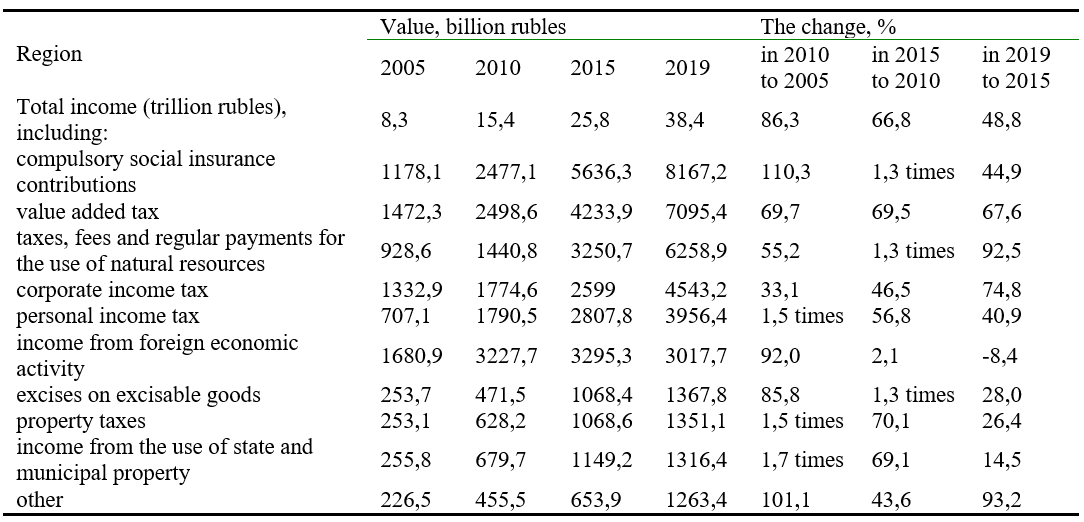

The total volume of revenues of the consolidated budget of the Russian Federation for the period under study increased to 38.4 trillion rubles, and for every 5 years between which the analysis is carried out, it shows high growth rates. So, its volume increased by more than 86% in 2005-2010, and there is a decrease in the growth rate to 67% and 49%, respectively, in subsequent periods, which allows us to conclude that over time there is a slowdown in the growth rate of the indicator. In the context of the main items of income of the consolidated budget of the Russian Federation, there is also a positive trend, with the exception of foreign economic activity in 2015-2019, where there was a decrease of 8.4%. In addition, in 2015, revenues from foreign economic activity amounted to 3.3 trillion rubles, which is only 2% higher than the 2010 level. This is due to the deterioration of the foreign policy situation against the background of the conflict with Ukraine in 2014, which had a significant negative impact on the country's foreign trade, the consequences of which have not yet been overcome. According to a number of authors (Tuktamysheva, 2021; Lektzian, & Mkrtchian, 2021), the deterioration of the foreign policy situation, which provoked the introduction of a number of anti-Russian sanctions and forced retaliatory measures, had a negative impact on many areas of the country's economy, but to the greatest extent on foreign trade. Formed over the years, international trade relations with the main partners were disrupted, as a result of which not only state revenues from foreign trade decreased, but also domestic enterprises, whose geography of activity went beyond the borders of the country, suffered, due to a decrease in sales.

In the period 2005-2010, the highest growth rates of budget revenues occurred in such areas as income from the use of state and municipal property, property taxes and personal income tax. In the next period, the most dynamic increase in revenues can be identified for excise taxes and taxes for the use of natural resources, while the increase in revenues decreased to 56% due to personal income tax, and decreased to 70% due to property taxes. In the period 2015-2019, there is an overall decrease in the growth rate of receipts in comparison with previous periods. As a result, the highest gain can be attributed to tax revenues for the use of natural resources. It is also worth noting that the volume of VAT revenues to the budget is growing at a steady pace in the study period, which vary within 67-70% (Table 1).

Table 1.

Dynamics of the consolidated budget revenues of the Russian Federation in current prices in 2005-2019

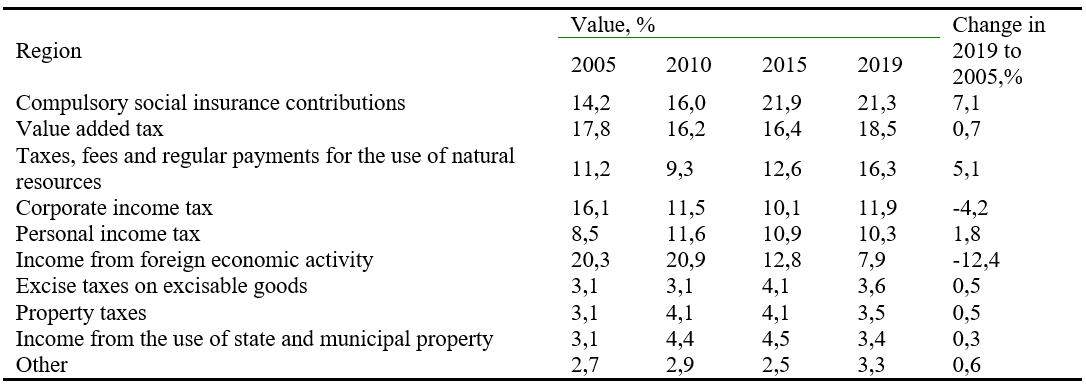

In the structure of revenues of the consolidated budget of the Russian Federation in 2019, the largest share began to fall on insurance premiums for compulsory social insurance, the share of which increased by more than 7% during the study period. The second position is occupied by VAT receipts, the share of which, although it decreased in 2010-2015, but increased to 18.5% in 2019, which is the highest value in the studied period. Taxes for the use of natural resources round out the top three in 2019 in the structure of budget revenues, the share of which is 16.3%.

In turn, a significant decrease in the share in the structure of budget revenues is noted for such an item as income from foreign economic activity: if the share of revenues was equal to 20.3% in 2005 and was the largest in the overall structure, then there was a decrease in the indicator to 7.9% by 2019, which is a natural consequence of the sanctions confrontation. The share of corporate income tax has also decreased, which was 16.1% in 2005, and has dropped to 10-12% since 2010. In general, it can be noted that the structure of the RF budget revenues is relatively stable for most items. At the same time, the increase in volumes occurred in such areas as insurance premiums for compulsory social insurance and taxes for the use of natural resources, while reducing the share of income from foreign economic activity and taxes on corporate profits (Table 2).

Table 2.

Structure of revenues of the consolidated budget of the Russian Federation in 2005-2019

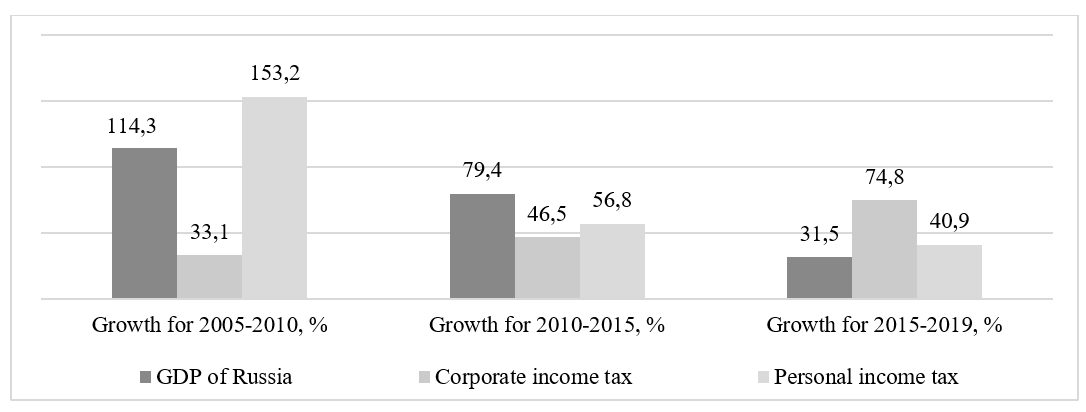

GDP is the main indicator characterizing the development of the economy, since, as noted by researchers (Mironov, & Konovalova, 2019; Skripkina, & Terekhov, 2016), it allows one to assess the phase of the economic cycle, the state and stability of the economy, and also to compare with the level of other countries. Even within the country, comparing the growth rate of the country's GDP with the growth rate of the consolidated budget of the Russian Federation in the context of the main items of tax revenues is of great importance, since it makes it possible to assess the trends taking place in the economy.

In the period 2005-2010, the growth rate of budget revenues due to personal income tax exceeded the growth rate of GDP, which indicates that the collection of taxes from individuals in this period of time grew more actively than the country's economy. In turn, the rate of increase in the volume of income tax in this period was slightly more than 30%, which is almost three times lower than the rate of GDP growth. For the period 2010-2015, the GDP growth rate, despite a decrease in comparison with the level of the previous period, exceeded the similar indicators for personal income tax and income taxes, which indicates that the economic situation was more favorable in this period of time. In turn, in the period 2015-2019, the growth rate of the country's GDP continued to decline, as a result of which the growth in 5 years amounted to only 32%, while the growth rate of budget revenues due to income tax increased compared to the previous period, becoming twice the level of GDP growth. The growth rate of personal income tax in the period 2015-2019 exceeded the level of GDP growth, although in comparison with previous periods, the downward trend of the indicator persists. The fact that the growth rate of personal income tax exceeds the growth rate of GDP indicates that the share of wages in the cost of goods produced in the country has increased, which is a negative trend (Figure 1).

Figure 1. Comparison of the GDP growth rates of the Russian Federation with the growth rates for the main income items of the consolidated budget of the Russian Federation in 2005-2019

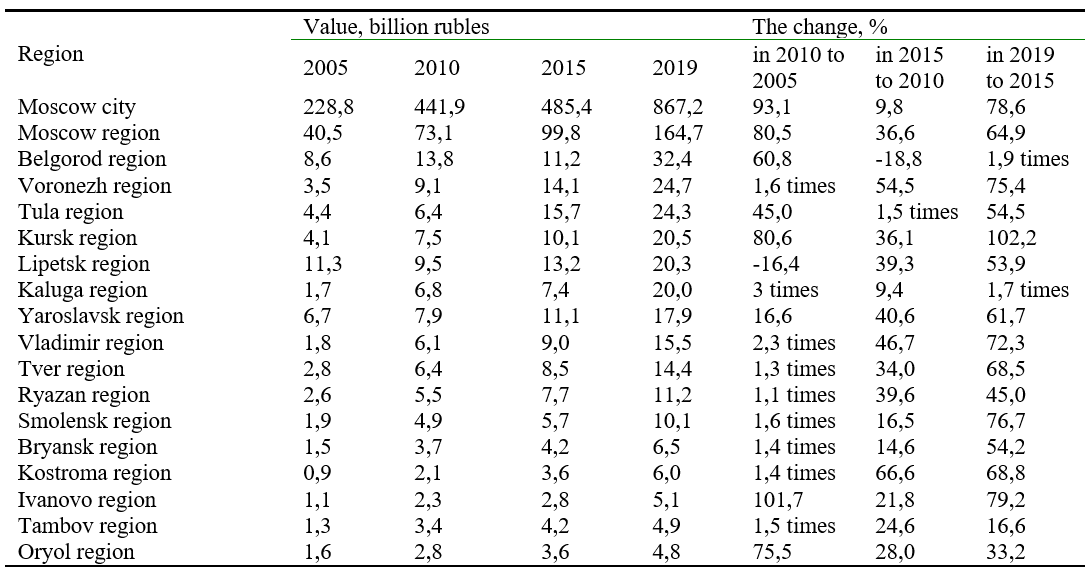

Assessment of the incomes of the consolidated budgets of the Central Federal District regions due to the income tax of organizations made it possible to reveal the existence of a significant differentiation in the volume of receipts between the regions, which is due to the inequality of their area and the number of functioning organizations. In addition, a comparison of the growth rates of the indicator over the years in the context of the regions of the Central Federal District showed the absence of a single trend, which indicates that the volume of income tax on profits is mostly due to intraregional factors. A significant increase in the volume of tax revenues from corporate income tax occurred in most regions of the Central Federal District (except for the Yaroslavl Region) over the period 2005-2010; negative dynamics (-16.4%) was outlined only in the Lipetsk region. A decrease in the growth rate compared to the level of the previous period was noted in the period 2010-2015, in most constituent entities of the district, and even negative dynamics (-18.8%) was outlined in the Belgorod region. In the last 5 years, there has been an increase in the growth rate of revenues to the consolidated budgets of the regions due to the corporate profit tax, and to the greatest extent - in the Belgorod (1.9 times) and Kaluga (1.7 times) regions (Table 3).

Table 3.

Dynamics of incomes of the consolidated budgets of the Central Federal District due to the income tax of organizations in 2005-2019

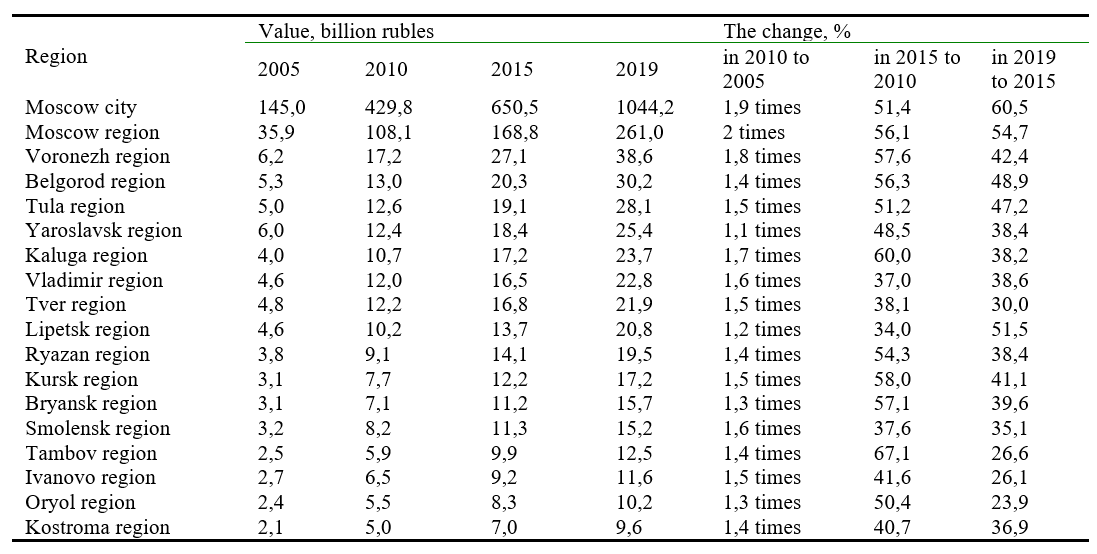

Assessment of the dynamics of personal income tax revenues to the consolidated budgets of the regions of the Central Federal District made it possible to reveal that there was a significant increase in budget revenues in all regions in the period 2005-2010; This is most likely due to the abrupt growth of the minimum wage (minimum wage) in 2009, when its size in the whole of the Russian Federation increased almost 5 times and amounted to 4,330 rubles in comparison with 800 rubles in the previous year. Since personal income tax is calculated from the wages of employees, such an increase in the minimum wage contributed to a manifold increase in the tax base, in connection with which the amount of tax revenues to regional budgets increased. In the period 2010-2015, there is a decrease in the growth rate of personal income tax revenues, which is also directly dependent on the minimum wage, since a significant part of the population has exactly the same amount of remuneration, in fact or nominally, receiving the rest of it “in an envelope” bypassing taxes. As a result, we can say that the growth of personal income tax revenues to the budgets of the regions of the Central Federal District is closely related to the annual indexation of the minimum wage. Since the moment of a sharp increase in this indicator in 2009 in subsequent years, its dynamics has been slow, then the increase in the volume of tax revenues is also carried out at a slower pace. The variation in the increase in tax revenues due to personal income tax is in the range of 34-67% for the period 2010-2015 in the context of the regions of the Central Federal District, and 24-61% for 2015-2019, which confirms the slowdown (table 4).

Table 4.

Dynamics of incomes of the consolidated budgets of the regions of the Central Federal District due to the income tax on personal income in 2005-2019

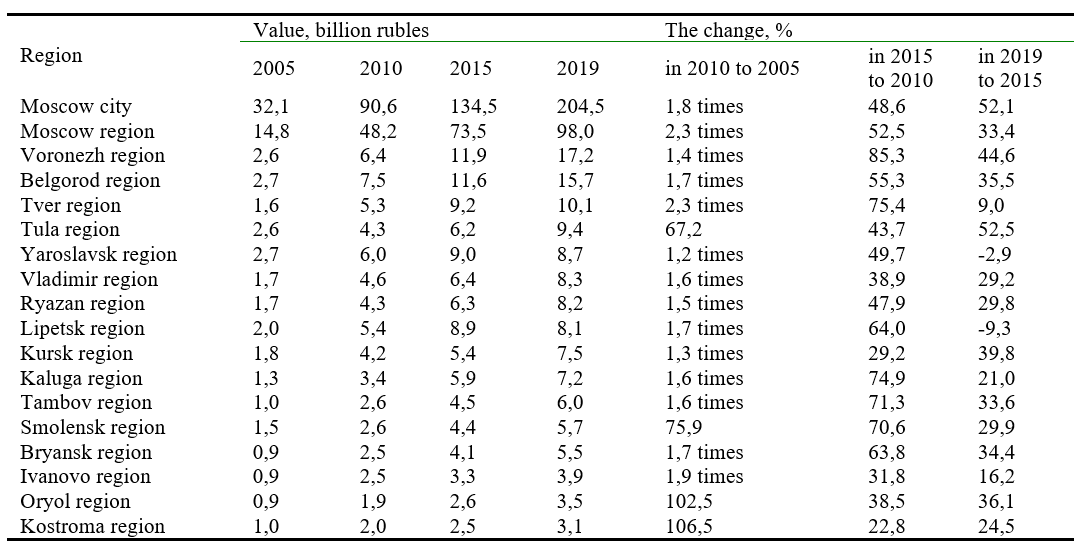

Similarly, in the period under study, the volume of tax revenues changed due to the collection of property tax (organizations and individuals). For the period 2005-2010, there has been a significant jump-like increase in the volume of receipts in most regions of the Central Federal District, which is most likely associated with a change in the procedure for determining the cadastral value of real estate, which directly depends on the size of the tax base. The transformations carried out contributed to the growth of the cadastral value of real estate as a result of its revaluation, which at unchanged rates naturally led to an increase in the volume of revenues to regional budgets. In subsequent years (2010-2015), the situation stabilized, as a result of which the growth rate of tax revenues decreased, but positive dynamics remained in all regions of the Central Federal District without exception. Over the period 2015-2019, the trend towards a decrease in the increase in the volume of tax revenues due to property tax continued, and there was a decrease in the volume of tax revenues under this item in a number of regions, such as the Lipetsk and Yaroslavl regions (Table 5).

Table 5.

Dynamics of incomes of the consolidated budgets of the Central Federal District due to property taxes in 2005-2019

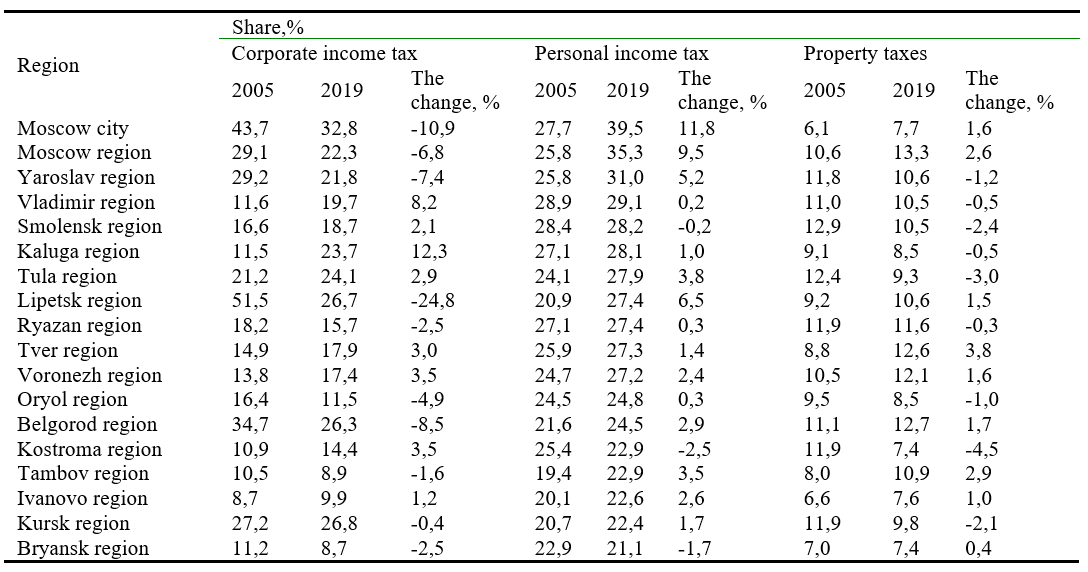

An assessment of the structure of the main types of tax revenues in the context of the regions of the Central Federal District revealed that in most regions the overwhelming share of tax revenues comes from personal income tax, and the highest rate is observed in Moscow (39.5%) and the Moscow region (35.3%), which is possible explain by a fairly high level of remuneration in the region. In the context of the regions of the Central Federal District, the variation in the share of personal income tax in the overall structure of revenues to the consolidated budget is within 21.1-39.5%. In addition, the change in the share of tax revenues from personal income tax in 2019 relative to 2005 has a positive trend in all regions of the Central Federal District, with the exception of the Smolensk, Kostroma and Bryansk regions (Table 6).

Table 6.

Change in the share of income of the consolidated budgets of the regions of the Central Federal District in the context of the main types of taxes in 2005-2019

The second in terms of specific weight are budget receipts from the profit tax of organizations, the share of which in the structure of income in 10 regions of the Central Federal District has a negative trend, while only in 8 regions there is an upward trend. During the study period, the share of corporate income taxes in the Lipetsk region decreased to the greatest extent, in which the indicator exceeded 50% in 2005, which is the highest value in the Central Federal District. By 2019, the decrease was almost half, as a result of which its value was 26.7%. In general, a significant differentiation in the share of revenues to the consolidated budgets due to income tax is noted in the context of the regions of the Central Federal District, and the indicator varies within the range of 8.7-32.8% in 2019. This indicates that the predominant formation of the revenue side of the consolidated budgets of the Central Federal District occurs at the expense of different sources of income, which is due to their economic characteristics. In turn, the share of property taxes in the total volume of tax revenues is the smallest in comparison with other types of taxes, and there are different dynamics in the context of the regions of the Central Federal District: while the dynamics are positive in other regions. Differentiation of the share of this type of tax revenues in the structure of budgets is less significant and is in the range of 7.4-13.3%.

In the formation of the revenue side of the budget of Russia at the current stage, there are two main elements - the labor and business components. According to a number of researchers (Alessandrini, 2021; von Schiller, 2018), personal income tax is the most promising tax, since its payers are the entire working-age population. This makes the volume of its receipts more stable, and the existing simple mechanism of collection creates fewer conditions for evasion of payment. It should be noted that today in the country in the conditions of active development of the shadow economy, the actual volume of tax revenues from personal income tax is significantly lower than the potential, since a significant part of the country's population receives wages "in an envelope". In recent years, there has been a slowdown in the growth rate of budget revenues at the expense of this tax, which is largely due to the overall low cost of labor in the market and the unwillingness of employers to actively raise wages, which is the basis for taxation (Gurvich, & Vakulenko 2017). The current situation is inextricably linked with the business component, since the deterioration of the economic situation contributes to a decrease in the profitability of enterprises, which affects not only wages, but also other elements of the production and economic chain, including the corporate income tax. Therefore, predicting the volume and creating conditions for replenishing the state budget from the profit tax is not promising in the context of the economic crisis (Alinaghi, Creedy, & Gemmell, 2021). At the moment, there are few industries in Russia that are not related to the raw materials and energy complex, which have managed to solve the problem of fully meeting domestic needs and move to an export model of functioning. For example, several subcomplexes of the agro-industrial complex (sugar beet and grain products) determine their development in this vein, and the business of these spheres can serve as sources for the growth of budget revenues (Golovin, Derkach, & Zyukin, 2020; Zyukin, Svyatova, & Soloshenko, 2016).

The practice of other countries confirms the importance of the formation of a rational system of taxation of individuals for the formation of a highly profitable state budget, since the income tax in the budgets of developed countries occupies a significant share (25-30%) of the revenues of the budgets, being a kind of its support (Zeynalova, 2020; Esneu, 2021). However, it is necessary to take into account the current tax rate in the country. In Russia, fixed rates are applied that do not depend on the amount of income, and such a system has shown its low efficiency in filling the revenue side of the state budget. In developed countries, progressive rates are used, which have shown high not only economic efficiency, but also social justice in relation to various categories of the population, including those with a low standard of living (Kazachenkov, 2020; Bontems, & Gozlan, 2018).

Conclusion

The total volume of revenues of the state budget of Russia has been actively growing in the past 15 years, which is due not only to qualitative changes, but also associated with inflationary processes in the economy. It should be noted that in the past 5 years, the growth rate of the revenue side of the state budget of the country has decreased in comparison with previous periods, which is most likely due to the deterioration of the economic situation against the backdrop of the next economic crisis. In 2019, more than half of the total volume of state budget revenues in total began to fall on insurance contributions for compulsory social insurance, value added tax and taxes, fees and regular payments for the use of natural resources, the volume of receipts of which to the state budget has been growing dynamically over the past 5 years. In turn, during the study period, there was a significant reduction in the share of income from foreign economic activity, the share of which in 2005-2010 exceeded 20%, and decreased to 12.8% by 2015, and to 7.9% by 2019, which is a consequence of political instability and the imposition of sanctions due to the conflict with Ukraine.

Comparison of the growth rate of Russia's GDP with the growth rate of income for the main types of taxes made it possible to establish that the growth rate of personal income tax at the beginning of the period under review was high, but had a steady downward trend, while the growth rate of corporate income tax, on the contrary, began to grow from over time and by 2019 exceeded the GDP growth rate. As a result, we can say that taxation in business is growing at a faster pace than the economy, and therefore the share of the pledged profit of organizations in the cost of production is increasing. Speaking about personal income tax, it is possible to reveal the opposite trend associated with a decrease in the share of wages in the structure of the cost of production; this, among other things, may also be due to the general low level of wages in the country and regions, the increase in which is due to indexation, and not to qualitative growth.

In the context of the regions of the Central Federal District, significant differentiation remains, both in the absolute value of the volume of budget revenues, and in the specific weight of one or another type of taxes. It is possible to distinguish a general trend towards a more active increase in the volume of receipts in 2005-2010 and a subsequent decrease in the growth rate over time, which is also associated with a general worsening of the economic situation. In the context of the regions of the Central Federal District, the overwhelming share of budget revenues comes from personal income tax, the volume of receipts of which is growing most dynamically, as a result of which its share varied from 21% to 40% by region in 2019. The share of income taxes in a number of regions significantly decreased as part of structural reforms in the revenue side of the consolidated budgets associated with more active growth of revenues from other sources, as a result of which the indicator varied between 8.7-32.8% in 2019.